After three consecutive record crops and the highest ever gross value for agricultural production, Australia is expecting smaller crop production in 2023-24.

Total winter crop production is forecast to drop 33% to 46.1 million tonnes, slightly below the 10-year average, according to the Australian Bureau of Agricultural and Resource Economics and Sciences (ABARES). Summer crop production is forecast to fall 27% to 3.8 million tonnes but is still slightly above the 10-year average.

Australia has a diverse agricultural sector, producing a wide range of crops, including significant amounts of wheat, barley and canola. After a three-year drought came to an end in 2020, many agricultural regions moved from very poor to very good conditions within the span of a season, ABARES said.

“The three successive years of record-busting wheat production have been extraordinary and established primarily on the back of three successive years of unusually high rainfall across most of Australia’s wheat producing regions,” said the Foreign Agricultural Service (FAS) of the US Department of Agriculture. “In addition, the higher-than-usual price for wheat encouraged high planted area and high input use to optimize yields.”

The nation achieved a record-setting A$94 billion in gross value for agricultural production in 2022-23. In the past 20 years, the gross value of agricultural, fisheries and forestry production has increased by 59%.

Exports are a significant portion of that value, accounting for 72% in 2022-23. In real terms, the value of agricultural exports has fluctuated between A$41 billion and A$71 billion since 2002-03.

“Grains, oilseeds and pulses have been the fastest-growing export segment, growing at an average annual rate of 10% in value terms between 2002-03 and 2021-22, followed by other horticulture and meat and live animals,” ABARES said.

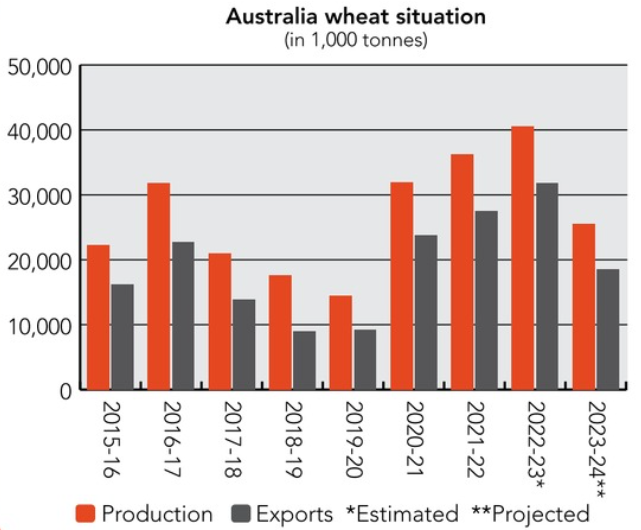

Credit: ©SOSLAND PUBLISHING CO.

Credit: ©SOSLAND PUBLISHING CO. Crop production, consumption

While improved prospects in southern cropping regions will offset reduced production in parts of New South Wales, Queensland and Western Australia, winter crop yields are still forecast to be below average, ABARES said. The area planted to winter crops fell year-on-year but was still historically high at 23 million hectares.

Wheat production is forecast to fall 37% to 25.5 million tonnes, 4% below the 10-year average while barley production is forecast to fall 24% to 10.8 million tonnes, also 4% below the 10-year average.

Canola production is expected to drop 33% to 5.5 million tonnes but is well above the 10-year average due to a planted area that is estimated to be the second highest on record.

With the last two years of exceptional rains and excellent commodity prices, farmers planted every available hectare to winter crops, the FAS said. This included areas that were earmarked for fallow and planting canola in the same field for consecutive years. A shift to a more typical rotation pattern, combined with canola prices falling back toward longer-term averages, is resulting in a reduced planted area, the FAS said.

The area planted to summer crops is down 21% to 1.2 million hectares, with production estimates also down 27% to 3.8 million tonnes. This is still slightly above the 10-year average of 3.5 million tonnes, ABARES said. Of the summer crops, sorghum is forecast to fall 45% to 1.5 million tonnes due to dry conditions and declining soil moisture levels during the early planting window.

Domestic consumption of wheat is estimated at 9 million tonnes in 2023-24, up from 8.5 million tonnes a year ago. Most of the wheat demand by the livestock industry is for beef cattle feedlots. In drought conditions, the beef cattle industry ramps up the volume of cattle in feedlots. There was a spike in feedlot usage in June, and the FAS said this was likely to continue well into 2023-24, prompting higher feed grain demand.

Australia on front lines of climate change

Australia on front lines of climate change

Wheat usage by the domestic flour milling industry is expected to remain unchanged from past years at 3.5 million tonnes, the FAS said. However, it noted with rapid population growth in 2023-24, there is a possibility for some growth in wheat consumption for milling in the near term.

ABARES said the gross value of agricultural production is forecast to fall by A$16 billion to $78 billion in 2023-24, still the third highest result on record. The drop is driven by lower crop production volumes due to reduced crop yields and global prices easing from recent highs.

Export focused

Australia is part of 17 free trade agreements, giving agricultural exporters an advantage in key destination markets, ABARES said. Still, the nation needs to continue to pursue improvements to market access, it said. As agricultural tariffs have fallen, non-tariff measures have risen.

“It is important to ensure that as the number of non-tariff measures rises, these are not used for protectionist purposes to create additional barriers to trade,” ABARES said.

Australia has more than 50 wheat export destinations, with five consistently big customers that have accounted for 55% to 70% of all exports, the FAS said. In the last two years, volumes have increased to all five destinations.

China is the largest destination by volume, with 26% of overall wheat exports in 2022-23. In the first part of 2022-23, South Korea has had the largest growth by volume, up almost 800,000 tonnes and a percentage increase of more than 180% from the same period a year ago.

“Indonesia and the Philippines also showed strong growth as wheat destinations for Australia,” the FAS said.

Australia is in a unique position to capitalize on key Asian export markets given its proximity to the region, ABARES said. Australia’s relatively low exchange rate also supports the value of exports in the short term as most agricultural exports are contracted in US dollars.

Due to the decrease in winter and summer crop production, ABARES lowered grain and oilseed export volumes for 2023-24. Wheat exports are expected to fall 35% to 20.9 million tonnes while canola is expected to be down 26% to 4.2 million tonnes.

During the last five years, about 75% of Australia’s canola exports have gone to the EU, primarily for the biodiesel market. Trade with United Arab Emirates, Japan and to a lesser degree the United Kingdom, have grown substantially since the rise in production, the FAS said.

Barley exports are estimated down 24% to 5.8 million tonnes and sorghum is expected to fall by 16% to 2.4 million tonnes.

“This is nonetheless 136% above the 10-year average, supported by strong demand from China,” ABARES said of sorghum exports.

Overall value of Australian crop exports is forecast to fall by 22% to A$39.5 billion. Values are likely to stay above average because of high exportable supply following record crop production in 2022-23.

Wheat, barley and canola are typically exported through the same ports and at similar times. The combination of strong global demand and record production of wheat and canola in 2022-23 pushed logistical export capacity to its limits.

The main bottleneck has been the transporting of grains from Western Australian regional receival points to port, and there have been substantial investments in upgrading some of these points over the last two years, the FAS said. Further upgrades are planned that will support future growth in grain exports.

Flour milling

While the wheat industry is export focused, flour produced in Australia is mostly used within the country. The flour milling industry has a long history of consolidation, peaking at more than 500 flour mills in the 1870s to about 30 mills now, according to the Australian Technical Millers Association.

Domestic consumption of flour is estimated at about 1.5 million tonnes with an additional 440,000 tonnes used for industrial purposes such as starch and gluten. Total flour production is estimated at 2.1 million tonnes and uses about 25% of Australia’s wheat production.

Large flour milling companies within Australia include Mauri, which is part of George Weston Foods, a division of Associated British Foods; Allied Pinnacle, owned by Nisshin Seifun Group, which includes Japan’s largest flour miller, Nisshin Flour Milling; and Australian family-owned Manildra Group.

Mauri is one of the oldest and largest cereal manufacturers in the Australasia region. Its parent company announced in 2022 plans for a new flour mill in Ballarat.

Allied Pinnacle operates seven mills and four mixing sites that manufacture a broad range of flour and cereal-based premixes.

Manildra operates four flour mills in the heart of the Australian wheatbelt, producing a full range of wheat flours, bakery mixes and special products such as durum semolina for pasta, for domestic and export markets. The mills process over 1 million tonnes of wheat per year.